- 2023 and 2024 revenues expected to grow by 20% and 17% on average globally year on year

- 48% of companies plan to increase staff numbers in the coming 6 months

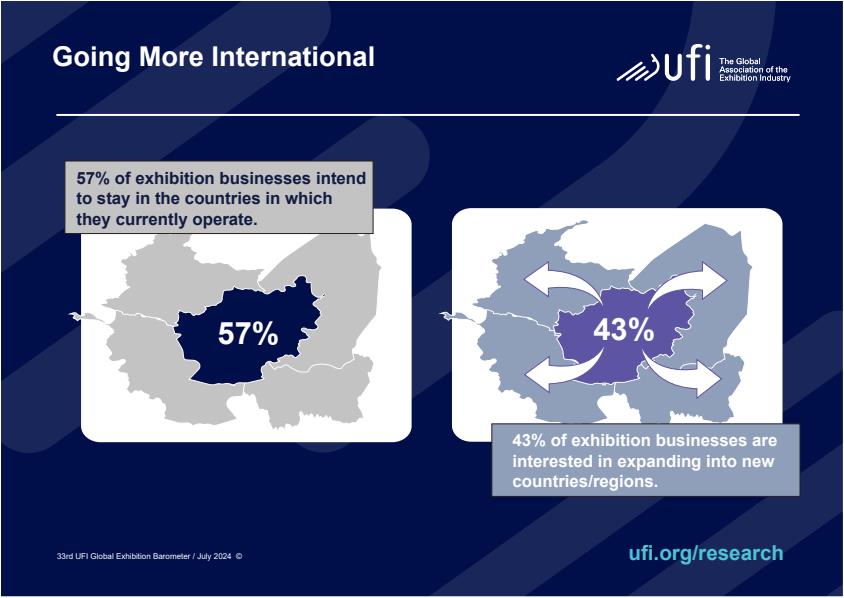

- 77% of companies plan to expand their scope of activities, and 43% declare an intention to expand into new countries and regions

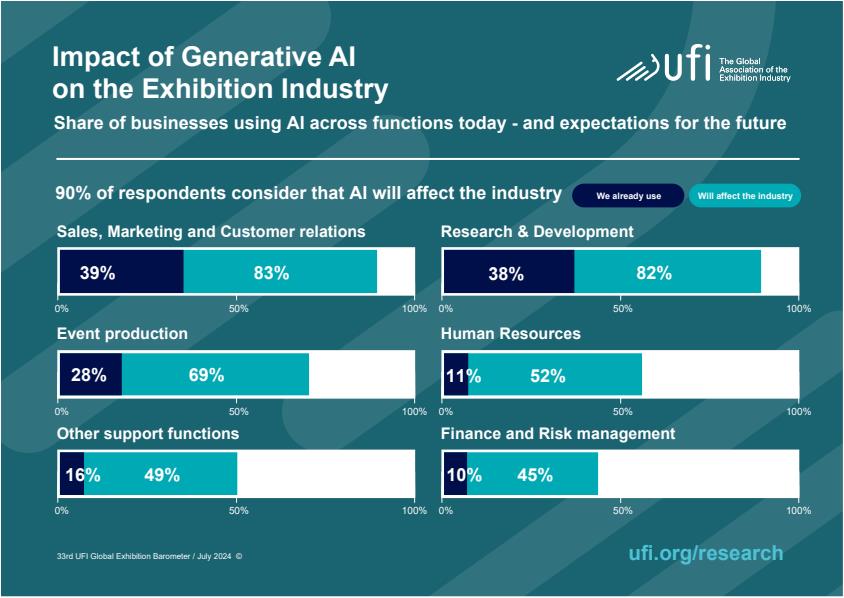

- Adaptation of generative AI continues to take hold across the industry

- Complete report includes dedicated profiles for 19 markets and regions, showcasing differences around the world

Paris – 8 August 2024: UFI, the Global Association of the Exhibition Industry, has released the latest 33rd edition of its flagship Global Exhibition Barometer report which takes the pulse of the industry.

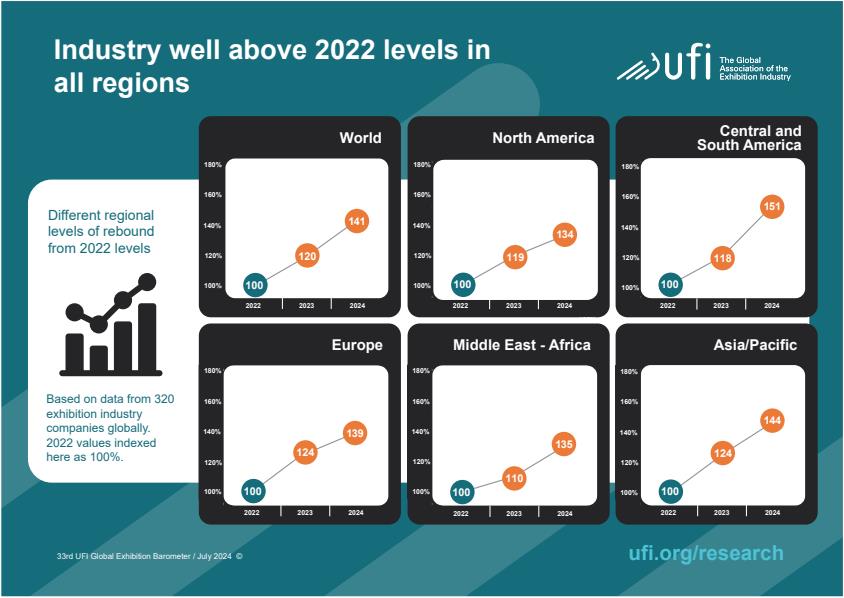

The results highlight that the exhibition industry will achieve record revenues globally in 2024, moving beyond the post-pandemic recovery that was achieved at the end of 2023 on average. 2023 and 2024 revenues are expected to grow by a respective 20% and 17% year on year.

Globally, 48% of companies declare that they plan to increase their workforce in the coming 6 months, while another 48% declare that they will keep current staff numbers stable.

“State of the economy in home market” is the most pressing issue (22% of answers globally), followed by “Global economic developments” (15% of answers).

There is a universal consensus that AI will affect the industry, with 90% of companies stating this, and a growing share of businesses reporting that they actively utilise this new technology.

“This edition of UFI’s flagship Barometer research confirms our early data from January that 2024 will be a record year for industry revenues globally. This edition shows how this growth translates into new jobs in our sector as well as in expansion plans from the majority of businesses – aiming both at new business activities as well as new geographies. Against a complex global backdrop, the global exhibition industry is bullish about its short and mid-term prospects”, comments Kai Hattendorf, Managing Director and CEO at UFI.

“The barometer also shows how 19 key exhibition markets and regions match up both against their respective regions and against the global averages. We have expanded this reporting further to make this data more easily accessible. There is no other research in this industry that allows for such level of comparison”, Hattendorf adds.

Size and scope

This latest edition of UFI’s bi-annual industry report was concluded in July 2024 and includes data from 453 companies in 68 countries and regions.

The study also includes outlooks and analysis for 19 focus countries and regions – Argentina, Australia, Brazil, China, Colombia, France, Germany, Greece, India, Italy, Malaysia, Mexico, Saudi Arabia, South Africa, Spain, Thailand, the UAE, the UK, and the USA – as well as five additional aggregated regional zones.

Operations

Globally, the level of operations in the first half of 2024 has picked up for half of the companies (4 out of 10 in Asia-Pacific, Central & South America and the Middle East & Africa; and 6 out of 10 in Europe and North America) while it was qualified as “normal” for one in three.

This trend will continue in the coming year with, on average, a percentage of companies reporting an increased activity ranging from 59% in North America to 50% in Asia-Pacific, 49% in the Middle East and Africa, and 48% in Central & South America and Europe, respectively.

Turnover and operating profits

Revenues increased by 20% on average in 2023, and this trend is expected to continue. In 2024, revenues are expected to grow again by an average of 17% year over year.

These general trends vary from one country to another:

- Revenues from 2023 compared to 2022 vary from 143% in Malaysia, 139% in Thailand, 132% in Argentina and the USA, to 105% in Spain, 103% in Brazil and 101% in Australia.

- Revenues from 2024 compared to 2023 vary from 148% in Colombia, 138% in Brazil, 123% in the UAE, to 106% in Germany, 105% in China and 98% in France.

In terms of operating profits for 2023, 61% of the companies declare an annual increase of more than 10%, and 27% declare a stable one. The same total of 88% applies to the 2024 operating profits, with 47% planning an annual increase of more than 10% and 39% a stable one.

The highest proportion of companies expecting an annual profit increase of more than 10% are in Malaysia (100%), Spain (83%) and Thailand (75%) for 2023, and Brazil (82%), the UK (69%) and Malaysia (58%) for 2024.

Workforce development

Globally, 48% of companies declare that they plan to increase their staff numbers, while another 48% declare that they will keep current staff numbers stable.

The highest proportion of companies planning to add staff are identified in Malaysia (91%), Brazil (75%) and the UAE (73%).

Most important business issues

This edition does not show significant changes when compared to the previous edition of the Barometer released six months ago:

- The most pressing business issue is “State of the economy in home market” (22% of answers globally – same as six months ago – and the main issue in all regions, except the Middle East and Africa, where it ranks second).

- Overall, “Global economic developments” come in as the second most important issue globally (15% of answers, compared to 17% six months ago), followed by “Geopolitical challenges” (14%, and the top issue for the Middle East and Africa) and “Competition from within the exhibition industry” (14%).

- “Internal management challenges” (11%), “Sustainability / Climate” (9%) and “Impact of digitalisation” (6%) follow.

An analysis by industry segment (organiser, venue only and service provider) shows no differences regarding the most pressing issue (“State of the economy in home market”), but the second and third ones vary: “Global economic developments” (17%) and “Geopolitical challenges” (16%) for organisers; “Competition from within the exhibition industry” (18%) and “Sustainability / Climate” (13%) for venues; “Competition from within the exhibition industry” (19%) and “Global economic developments” (15%) for service providers.

Current strategic priorities

In all regions, a large majority of companies intend to develop new activities, either in the classic range of exhibition industry activities (venue/organiser/services), outside of the current product portfolios, or in both areas: 69% in Asia-Pacific, 74% in North America, 75% in Central & South America, 83% in Europe and 84% in the Middle East & Africa.

In terms of geographic expansion, 43% of companies declare an intention to develop operations in new countries and regions.

Generative AI applications

Globally, there is an overwhelming consensus that AI will affect the industry, with 90% of companies stating this.

The areas expected to be most affected by the development of AI are the same in all regions: “Sales, Marketing and Customer Relations” (83% globally), “Research & Development” (82%) and “Event Production” (69%).

These are precisely the areas where generative AI applications are already mostly used, and in all regions (39%, 38%, and 28% globally, respectively).

Background

The 33rd Global Barometer report, concluded in July 2024, provides insights from 453 companies, across 68 countries and regions. It was conducted in collaboration with 32 associations:

AAXO (The Association of African Exhibition Organizers) and EXSA (Exhibition and Events Association of Southern Africa) in South Africa, ABEA (Australian Business Events Association), ABEOC (Associao Brasileira de Empresas de Eventos) and UBRAFE (União Brasileira dos Promotores Feiras) in Brazil, AEFI (Italian Exhibition & Trade Fair Association) in Italy, AEO (Association of Event Organisers) in the UK, AFE (Spanish Trade Fairs Association) in Spain, AFECA (Asian Federation of Exhibition & Convention Associations) in Asia, AFEP (Asociacion de Ferias del Peru) in Peru, AFIDA (Asociación Internacional de Ferias de América) in Central & South America, AIFEC (Asociacion Colombiana de la Industria de Ferias, Congresos, Convenciones y Actividades Afines) in Colombia, AKEI (The Association of Korean Exhibition Industry) in South Korea, AMEREF (Asociacion Mexicana de Recintos Feriales) and AMPROFEC (Asociación Mexicana de Profesionales de Ferias y Exposiciones y Convenciones) in Mexico, AOCA (Asociación Argentina de Organizadores y Proveedores de Exposiciones, Congresos, Eventos y de Burós de Convenciones) in Argentina, APPCE (Asociación Panameña de Profesionales en Congresos, Exposiciones y Afines) in Panama, AUDOCA (Asociación Uruguaya de Organizadores de Congresos y Afines) in Uruguay, HKECIA (Hong Kong Exhibition and Convention Industry Association) in Hong Kong, IECA/ ASPERAPI (Indonesia Exhibition Companies Association) in Indonesia, IEIA (Indian Exhibition Industry Association) in India, JEXA (Japan Exhibition Association) in Japan, MFTA (Macau Fair & Trade Association) in Macau, MACEOS (Malaysian Association of Convention and Exhibition Organisers and Suppliers) in Malaysia, MECA (Myanmar Exhibition and Conference Association) in Myanmar, PEIFE (Professional Events Industry Association Saudi Arabia) and SCEGA (Saudi Conventions & Exhibitions General Authority) in Saudi Arabia, SECB (Singapore Exhibition & Convention Bureau) in Singapore, SISO (Society of Independent Show Organizers) for the US, SOKEE (Greek Exhibition Industry Association) in Greece, TEA (Thai Exhibition Association) in Thailand, and UNIMEV (French Meeting Industry Council) in France.

“Thank you to all the partners who help us reach good levels of answers, leading to valuable snapshots for many markets”, says Christian Druart, UFI Research Manager.

In line with UFI’s objective to provide vital data and best practices to the entire exhibition industry, the full results can be downloaded at www.ufi.org/research.

The next UFI Global Exhibition Barometer survey will be conducted in December 2024.

Attachments:

{kind=link}

{kind=link}

{kind=link}

{kind=link}